That quiet necessity makes the ultrasound gel market predictable in the best way: demand tracks procedure volume almost directly. As diagnostic imaging expands into outpatient clinics, emergency departments, and physical therapy practices — and as handheld devices push ultrasound beyond the radiology suite — gel consumption follows.

This report covers current market valuation, growth forecasts heading into 2026, the key drivers and restraints shaping the category, segment dynamics, regional trends, and what procurement managers and clinic owners should prioritize when sourcing gel this year.

Key Takeaways

- The global ultrasound gel market ranges from $97.9M (2022 baseline) to an estimated $116–124M+ by 2025–2026, depending on the forecast source

- Non-sterile gel holds ~73% market share; sterile single-use formats are the fastest-growing segment

- North America leads at approximately 39–40% of global revenue; Asia Pacific is growing fastest

- Chronic disease growth, outpatient care expansion, and POCUS adoption are driving demand

- Gel-free probe technology remains a limited, high-cost niche with no significant near-term market impact

What Is Ultrasound Gel? Composition, Function, and Clinical Use

How It Works

Ultrasound waves travel poorly through air. Even a thin air gap between a transducer and skin disrupts signal transmission enough to degrade image quality noticeably. Ultrasound gel solves this by filling that gap with a water-based conductive medium that acoustically matches soft tissue, allowing sound waves to pass through with minimal loss.

A 2022 peer-reviewed formulation study confirmed this mechanism: ultrasound gel replaces air between the transducer and skin because ultrasound waves have difficulty traveling through air. The gel acts as an acoustic bridge, not a signal amplifier. Formulation precision determines how closely the gel's acoustic impedance matches soft tissue — which directly affects image clarity.

Standard Formulation

Professional ultrasound gels share a core ingredient set, though exact formulations vary by manufacturer and product type. Common components include:

- Water — the primary base

- Carbomer (Carbopol 940) — primary gelling and thickening agent

- Propylene glycol or monopropylene glycol — additional viscosity modifier

- Preservatives (such as phenoxyethanol) — antimicrobial protection in multi-use formats

- Optional colorants (FD&C Blue #1 is used in some commercial products per Medline MSDS documentation)

The finished gel must be clear, non-staining, and hypoallergenic — viscous enough to stay on the transducer without running.

For therapeutic ultrasound applications involving extended contact, non-residue properties and skin comfort carry more weight than they do in brief diagnostic scans.

Where It's Used

| Setting | Primary Application |

|---|---|

| Diagnostic imaging (OB/GYN, cardiac, abdominal) | Transducer coupling for imaging clarity |

| Physical therapy and rehabilitation | Therapeutic ultrasound tissue treatment |

| Emergency medicine / POCUS | Rapid bedside assessment with handheld devices |

| Ambulatory and outpatient clinics | Routine and follow-up imaging |

Each setting carries different requirements. Emergency use may tolerate standard non-sterile gel. Procedures near open wounds or involving needle guidance require sterile single-use formats. Physical therapy sessions benefit from gel that stays in place during extended treatment time.

Ultrasound Gel Market Size and Forecast: Where the Market Stands Heading Into 2026

Current Valuation

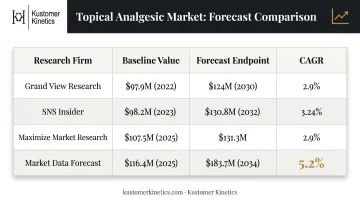

Multiple independent research firms have published estimates, and the figures span a meaningful range:

| Source | 2022–2025 Baseline | Forecast | CAGR |

|---|---|---|---|

| Grand View Research | $97.9M (2022) | $124.0M by 2030 | 2.9% |

| SNS Insider | $98.2M (2023) | $130.8M by 2032 | 3.24% |

| Maximize Market Research | $107.5M (2025) | $131.3M (endpoint) | 2.9% |

| Market Data Forecast | $116.4M (2025) | $183.7M by 2034 | 5.2% |

The conservative baseline, Grand View Research's $97.9M in 2022 rising to $124M by 2030, is the most widely cited figure. More recent reports (2025) place the current market notably higher, suggesting the baseline has already been exceeded.

What a 3% CAGR Actually Means for Buyers

A roughly 3% annual growth rate is modest by pharmaceutical standards. For gel procurement, that translates to:

- Stable pricing with gradually rising total demand as procedure counts climb

- Predictable annual budgets for procurement planners — no sudden cost spikes

- Growing order volumes for suppliers without significant margin pressure

The Procedure Volume Engine

The demand case for gel tracks directly with ultrasound procedure growth. NHS England's 2024/25 Diagnostic Imaging Dataset recorded 11.5 million diagnostic ultrasonography procedures out of 46.1 million total imaging tests — making ultrasound the second most common imaging modality in that system. That single-country figure illustrates the procedure density that drives gel consumption.

Affordable Devices Are Widening the Buyer Base

The point-of-care ultrasound (POCUS) market grew from $3.6B in 2022 to $4.0B in 2024 as handheld devices became affordable enough for emergency departments, rural clinics, and outpatient practices. Each new device deployment creates a recurring gel purchase requirement. This expansion beyond hospital radiology departments is a genuine growth accelerator for the consumable category.

Primary Restraint: Gel-Free Technology

CIVCO markets its Envision probe covers for gel-free ultrasound procedures. No authoritative public data yet confirms mainstream adoption timelines or price parity with gel. At current pricing, gel-free options remain a niche solution: a constraint worth monitoring, not an immediate replacement threat.

Key Growth Drivers Fueling the Ultrasound Gel Market

Rising Chronic Disease Burden

Cardiovascular disease, kidney and gallbladder disorders, and vascular complications all depend heavily on ultrasound for diagnosis and monitoring. The CDC reported 919,032 cardiovascular disease deaths in the U.S. in 2023 — roughly one every 34 seconds. The diagnostic workup behind those patient volumes generates substantial ultrasound procedure counts, and each scan requires gel. As chronic disease prevalence rises and clinical monitoring intensifies, that demand compounds year over year.

Physical Therapy as an Underreported Demand Channel

Therapeutic ultrasound — used for tissue healing, inflammation reduction, and musculoskeletal pain management — requires gel application before every session. The U.S. physical therapy services market reached $52.3B in 2025, with thousands of clinics conducting multiple ultrasound therapy sessions daily. Market research often focuses on diagnostic imaging, but PT clinics are a consistent, high-frequency gel consumer — one that procurement planners frequently undercount.

Prenatal and Obstetric Screening

The WHO recommends at least one ultrasound scan before 24 weeks of gestation as standard prenatal care. Globally, improving access to prenatal services — particularly in developing markets — is adding procedural volume to the OB/GYN segment, which was already one of the highest-frequency diagnostic ultrasound categories.

Infection Control Driving Sterile Format Adoption

A CDC MMWR report documented a Burkholderia stabilis outbreak linked to contaminated ultrasound gel. That documented outbreak is a direct reason AIUM's 2025 guidelines now recommend sterile single-use gel packets when infection risk is present. Heightened infection control awareness pushes facilities toward single-use formats, increasing per-patient gel spend even where total procedure counts stay flat.

Outpatient and Home Care Expansion

The AHA's 2024 market scan projected outpatient volumes rising 17% to 5.82 billion visits. More patients receiving care outside hospital walls means gel is consumed across a wider range of settings:

- Ambulatory surgical centers

- Urgent care clinics

- Home health and mobile care environments

This distribution shift moves consumption away from centralized hospital procurement and into smaller, more frequent purchasing channels.

Market Segmentation: Sterile vs. Non-Sterile, and Who's Buying

Type Segmentation

Non-sterile gel holds approximately 73.4% of global market share (Market Data Forecast, 2022). It's the standard format for routine external imaging — abdominal scans, echocardiography, prenatal monitoring — where the skin is intact and contamination risk is low. Multi-dose bottles are cost-effective and practical for high-volume settings.

Sterile gel, packaged in individual single-use sachets, is required for:

- Procedures near open wounds or broken skin

- Ultrasound-guided needle insertion or aspiration

- Intraoperative or invasive-adjacent applications

Sterile gel costs more per unit, but in these clinical contexts, it's not optional. Maximize Market Research projects the sterile segment growing at 8.18% CAGR — nearly three times the overall market rate.

That cost difference also affects how facilities manage non-sterile stock. Most infection control guidance — including UKHSA's 2025 recommendations and UCSF's facility protocol — specifies that opened non-sterile gel bottles should be discarded within 28–30 days, regardless of remaining volume. Facilities that don't track opening dates face both compliance and contamination risk.

End-Use Breakdown

- Hospitals — Largest segment at approximately 56.9% of revenue (2022); driven by high patient volume, complex imaging protocols, and centralized procurement

- Clinics and diagnostic centers — Fastest-growing segment, supported by affordable handheld devices and rising outpatient care volumes

- Ambulatory surgical centers — Growing channel, particularly for sterile gel demand

- Physical therapy and sports medicine practices — Consistent per-unit buyers due to high session frequency; frequently undercounted in aggregate market data despite steady demand

Practical Guidance for Procurement

Understanding end-use patterns helps procurement teams match the right format to the right setting:

| Buyer Type | Recommended Format |

|---|---|

| High-volume hospital imaging | Bulk non-sterile bottles or gallons |

| PT / rehab / chiropractic clinic | Multi-use bottles; gallon with pump dispenser |

| Invasive procedure / wound-adjacent | Sterile single-use sachets only |

| Emergency / POCUS setting | Non-sterile for intact skin; sterile sachets when skin integrity unclear |

Regional Breakdown: Where Growth Is Fastest

| Region | Market Position | Key Metrics | Primary Driver |

|---|---|---|---|

| North America | Largest (39–40% of global revenue) | U.S. dominant national market | High healthcare spend, dense hospital infrastructure |

| Asia Pacific | Fastest-growing | $29.7M (2023) → $37.2M (2030), 3.3% CAGR | Government investment, rising middle-class patient populations |

| Europe | Second-largest | 11.5M ultrasound procedures (NHS England, 2024/25) | Procedure-dense mature health systems |

| Latin America / MEA | Emerging long-term | Limited gel-specific data available | Healthcare modernization expanding ultrasound access |

North America commands roughly 39–40% of global revenue, with the U.S. as the clear national leader. High healthcare expenditure, dense hospital networks, and expanding community clinic infrastructure all reinforce that position — and show no signs of eroding.

Asia Pacific is the region to watch. Grand View Research projects the APAC market climbing from $29.7M in 2023 to $37.2M by 2030 at a 3.3% CAGR, outpacing the global average. Several factors are pushing that growth:

- Large unmet healthcare needs across rural and underserved populations

- Government-led investment in hospital and clinic infrastructure

- Rising middle-class patient volumes willing to pay for diagnostic services

- Domestic manufacturers in India and China lowering local price points

Europe holds second place, with steady gel demand tied directly to high procedure volumes — the NHS England 11.5 million ultrasound procedures recorded in 2024/25 being a reliable indicator of how consistent that baseline consumption is.

Key Players and What Defines a High-Quality Ultrasound Couplant

The Competitive Landscape

The ultrasound gel market is fragmented. Established names commonly cited across market research include Parker Laboratories, Medline Industries (distributor of Aquasonic 100), H.R. Pharmaceuticals, ECO-MED, and Compass Health Brands. Competition centers on formulation quality, packaging options, sterility formats, shelf life, and private-label availability — not dramatic product differentiation.

Formulation Quality: What Practitioners Should Prioritize

When evaluating gel suppliers, the following properties matter most:

- Acoustic coupling performance — The gel must transmit sound without signal loss; FDA 510(k) documentation for professional gels specifies acoustic impedance (Parker's Aquasonic is documented at ~1.60) and sound speed (~1,516 m/s)

- Appropriate viscosity — Thick enough to stay on the transducer; not so thick it impedes movement

- Hypoallergenic formulation — Non-sensitizing, non-irritating for repeated skin contact

- Non-staining and fragrance-free — Essential in clinical environments

- Shelf life — Parker's Aquasonic IFU documents a 5-year shelf life from manufacture under proper storage conditions

- Warming compatibility — Relevant for therapeutic ultrasound settings where gel warmers are used

One manufacturer that meets these criteria is Kustomer Kinetics.

Kustomer Kinetics: Sonic Scan™ and Ultra Gel™

For physical therapy clinics, chiropractic offices, sports medicine facilities, and diagnostic imaging centers, Kustomer Kinetics, based in Arcadia, CA, manufactures two ultrasound couplants:

- Sonic Scan™ — Diagnostic ultrasound scanning couplant, formulated with a non-greasy, hypoallergenic profile for clinical imaging in hospitals, OB/GYN, cardiology, and imaging centers

- Ultra Gel™ — Therapeutic ultrasound couplant built specifically for PT, chiropractic, sports recovery, and rehabilitation clinic applications

Both products are available in 16 oz bottles, gallon containers, and 4-gallon cases — with pump dispensers for chairside use. Kustomer Kinetics also offers a private-label program, letting clinic chains, distributors, and OEM equipment manufacturers put their brand on professionally manufactured couplants. GPO and wholesale pricing tiers are available for high-volume buyers.

Kustomer Kinetics manufactures all products in Arcadia under cGMP-aligned practices, with full MSDS documentation available. Clinics and distributors interested in volume pricing or private-label arrangements can reach the company at 626-445-6161.

Frequently Asked Questions

Frequently Asked Questions

What is the best gel for ultrasounds?

The best ultrasound gel matches the transducer type, transmits sound without interference, and meets the sterility requirements of the procedure. For clinical and therapy settings, Kustomer Kinetics' Sonic Scan (diagnostic) and Ultra Gel (therapeutic) are purpose-formulated for these demands.

What is the price of ultrasound gel?

Pricing varies by format and volume. Bulk non-sterile gallons are the most cost-effective option for high-volume clinical use; sterile single-use sachets carry a significant per-unit premium. Request volume-based quotes directly from professional suppliers — pricing structures differ by pack size, MOQ, and purchasing channel.

What is ultrasound gel made of?

Most formulations combine water, carbomer (Carbopol 940) for thickening, propylene glycol for viscosity, and preservatives such as phenoxyethanol. The formulation is water-soluble, non-toxic, and designed for safe repeated skin contact. Some commercial products include colorants; clinical-grade options are typically fragrance-free.

Is ultrasound gel sterile or non-sterile?

Both formats exist. Non-sterile multi-use bottles are standard for routine external imaging on intact skin. Sterile single-use sachets are required for procedures involving open wounds, needle guidance, or invasive-adjacent applications. Facilities should maintain both formats and use sterile packets whenever skin integrity is compromised.

How long does ultrasound gel last after opening?

Opened non-sterile bottles should be discarded within 28–30 days, per UKHSA 2025 guidance and standard facility protocols. Unopened products typically carry a shelf life of up to 5 years when stored appropriately.

What is driving growth in the ultrasound gel market?

Key drivers heading into 2026 include rising procedure volumes, expanding outpatient infrastructure, and growing chronic disease burdens requiring regular imaging. Affordable POCUS devices are also pushing ultrasound into non-hospital settings, while stricter infection control protocols are increasing per-patient sterile gel consumption.